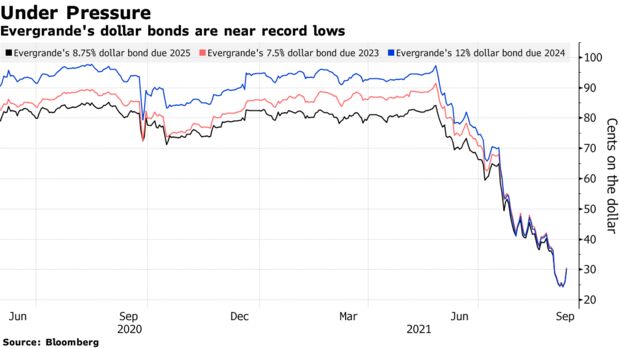

China Evergrande Group may undergo one of the country’s biggest-ever debt restructurings, if the developer’s distressed-level bond prices are any indication.

It’s “almost unavoidable,” said Nomura International Hong Kong Ltd. credit analyst Iris Chen. Her base case is a government-supervised deal that ensures Evergrande delivers homes and pays suppliers, where dollar debt investors would get 25% of their money back. Luther Chai, a senior research analyst at CreditSights Singapore LLC, also says Evergrande will default and enter restructuring. That risk is being priced in, with many of Evergrande’s dollar bonds trading near 30 cents.

How Defaults in China Are Reshaping Its Credit Market: QuickTake

Debt delinquencies at developers the size of Evergrande are so rare in China that investors, analysts and regulators would only have a few case studies to go on. Kaisa Group Holdings Ltd. in 2015 became the first Chinese builder to default on dollar bonds. The restructuring of another, China Fortune Land Development Co., is currently under negotiation.

Any disorderly failure by the firm may pose a threat to the financial system. The lack of clear precedents also means Chinese authorities have yet to test mechanisms in solving a debt problem quite like Evergrande, which has more than $300 billion in liabilities.

Evergrande didn’t immediately respond to a request for comment on its financial health.

Regulators in Beijing have signed off on an Evergrande proposal to renegotiate payment deadlines with banks and other creditors, paving the way for a temporary reprieve, a person familiar with the matter said last week.

Below are three potential scenarios.

Base case

Evergrande restructures its debt and bondholders recover a portion of their funds. This would be an “orderly wind down,” says Omotunde Lawal, head of Barings LLC’s emerging-market corporate debt group. There may be some contagion across China’s property issuers at first, according to Nomura’s Chen, though sentiment would improve as a key overhang would be removed. She expects only a 5% recovery rate for investors in Evergrande unit Scenery Journey Ltd.

It’s essential that normal operations continue after any potential default of a Chinese developer, wrote Morgan Stanley analysts led by Kelvin Pang in an Aug. 18 note. In other words, construction projects would be completed and homes would be delivered. And because dollar debt funding is “crucial” for developers, a defaulted property developer may not necessarily favor onshore creditors over those offshore, according to Morgan Stanley.

The government would likely be involved in a restructuring process, CreditSights’s Chai said in emailed comments, though Beijing is unlikely to prevent a default or be seen as a creditor of last resort. The Communist Party’s involvement would come later, allowing it to address moral hazard in the credit market while ensuring that any potential social, financial or economic fallout is limited.

Blue sky

A complete or partial takeover by a state-owned enterprise is another possibility, though Nomura’s Chen assigns a low probability to this scenario. Evergrande could also sell its listed assets at better prices if market conditions improve, says Chen, which she predicts would give bondholders a recovery rate of 30% or more.

Evergrande could buy some time to improve its liquidity over the next year, according to Chai at CreditSights. In this scenario, Evergrande would repay some of its nearest-term dollar bonds upon maturity. The developer has two sizeable dollar bonds due over the next 12 months, or a combined $3.5 billion to pay.

Evergrande is looking to sell non-core assets, which could help service upcoming debt obligations, though it last month warned that it risks default if its efforts fall short.

Nightmare

The day’s biggest storiesGet caught up with the Evening Briefing. Email By submitting my information, I agree to the Privacy Policy and Terms of Service and to receive offers and promotions from Bloomberg.

Liquidation is a scenario where bondholders may get close to nothing. This is unlikely, says CreditSights’s Chai, because it would “wreak havoc across China’s property and banking sectors, as well as related companies such as Evergrande’s suppliers.” Morgan Stanley analysts say “all parties are incentivized to avoid a liquidation scenario” in the restructuring of any Chinese property developer. Chairman Hui Ka Yan, who controls more than 70% of Evergrande’s equity — would lose a significant portion of his wealth.

Another negative scenario would involve Evergrande bringing some of its off-balance sheet debt — which may include pledged assets — back into the books, according to Nomura’s Chen. These assets could have priority over the dollar bonds in a recovery and if the off-balance sheet debt is higher than expected, bondholders could get less than 15% of their money back.

Nobody wants a messy process, says Barings’s Lawal. Property accounts for a significant portion of household assets in China and is a key component of President Xi Jinping’s “common prosperity” push to redistribute wealth.

“We always viewed the likelihood of a disorderly default to be low,” Lawal said via email last week. “Given how much of a nationwide player Evergrande is and the impact for homeowners with deposits and suppliers nationwide — the impact would quite likely be rather disruptive.”

— With assistance by Emma Dong